By Thomas McLamb

From 1932-1945, FDR responded to the Great Depression by way of the New Deal to temporarily put a bandage on the crises of capital. This creation of the American Welfare State served as the response to the occasional short-term downturns of capitalist expansion. From FDR’s term until the Oil Crisis in the early 70s, the United States capitalist system enjoyed a period of steady growth and a stable rate of profit, whose occasional declines were solved by way of a variety of government programs that sent one clear message; the government existed to serve the people.

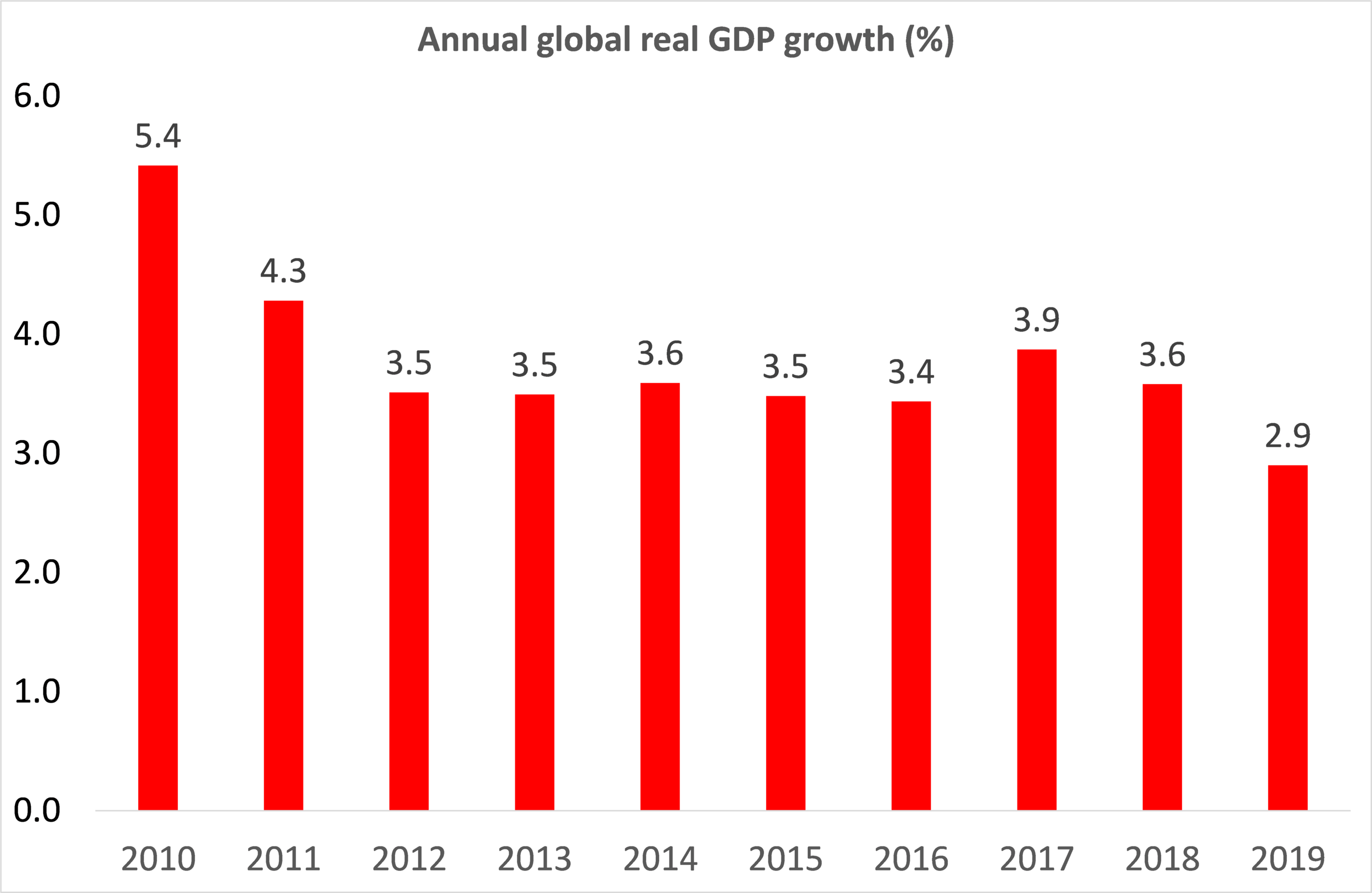

When Nixon took office, the processes of persistent economic inflation became apparent, indicating that this long period of economic expansion and stability was changing. That said, Marxist analyses of economic patterns of expansion, contraction, and long-term growth should stray away from the use of inflation as an economic pattern. Inflation is merely the process by which bourgeois economists summarize the degeneration of working-class buying power and strengthening of capitalist class buying power. In one short phrase – the dollar is fundamentally worth less to the worker than it is to the capitalist. While the capitalist is able to purchase more money with less, an exponential process depending on how much capital has been accumulated, the worker is dependent on purchasing essential life commodities, healthcare, food, housing, etc. with their dollar; the worker does not enjoy the luxury of purchasing more money with less, a process that inevitably leads to the phenomenon neoclassical economists refer to as inflation. Regardless of the actual relationship of inflation and the working-class, the aforementioned cycle of profits and growth from the post-war periods came to an end with the ’73-75 recession. The long wave of capitalist expansion had begun to wane, signaling the forthcoming period of long-term stagnation of working-class wages still underway today.

The end of the doctrine of the Welfare State led directly into a new doctrine of economic policy. The dominant economists of the period suggested that government welfare was wasteful and inefficient, that the occasional patterns of economic recession could be solved by allowing the markets to regulate themselves. The general assumption of these economists, i.e. Friedman et. al., was that government welfare resulted in an exponential process of inflation that could be remedied by a revival of liberal economics. This renascent adoration of laissez-faire capitalism came to serve as the genesis and framework of neoliberalism – the doctrine of cutting government expenses by any means necessary. Following the birth of neoliberalism, austerity quickly set in. The government responded to crises by allowing the bottom to hit the bottom, and externalizing and outsourcing previously domestic forms of labor that had now suffered from a declining rate of profit.

Alongside the externalization and outsourcing of labor from the United States, a process that signaled the shift of the U.S. to a strictly service and information economy, came a renascent nationalism and patriotism within the United States. This renascent nationalism served as the popular justification for the endless oil wars in the middle east, the incessant and undemocratic CIA-backed military coups in Latin America, and the continuous starving acts of tariffs and embargoes against foreign governments who refused to kneel to the imperialist war cry of neoliberalism. In industries where the rate of profit waned in the United States, the government merely cut popular welfare programs to fund the imperialist war machine to appropriate resources, governments, and economies of foreign governments, continuing the accumulation of capital and comfortable seat of influence of America.

Away from the wars, coups, and starvation acts outside of American borders, American workers waded through an ever-changing industry of employment in the United States. The neoliberal response to the discovery of ‘inflation,’ better understood as another symptom of the declining rate of profit, resulted in the same outcome the neoliberal economists and politicians believed they would be avoiding – a period of long-term stagnation of working-class wages and the devaluation of the buying-power of the working-class by large-scale privatization and imperialist efforts to sustain the total economic growth of the U.S. economy. Of course, these solutions worked to create more wealth than ever and higher profitability that ever before in the United States, but the measure of the total economy and its exponential growth ignores the continuous struggle of the non-propertied class. Marx’s theories of surplus value provide us with the truth that all profit is derived solely from labor. With that understood, wherever labor costs can be reduced, they will be, and profits will increase. Additionally, the buying-power of those wages themselves have been structurally diminished long-term by the neoliberal doctrine. This process of the stagnation of working-class buying power can be observed in the history of wages since the beginning of the neoliberal period. Real per capita wealth in the U.S. has more than doubled since 1964 while average real wages have barely increased. From 1964 to 2018, the buying power of the average worker in the United States increased by only 11.7% while the actual average wages themselves have increased by 806%. This mass rate of inflation is not an aberration of capitalist market economies – it is precisely a function of the long and short waves of capitalist development; all of which is accelerated and exaggerated by neoliberal austerity.

Over the past 50 years, over 90% of all growth in income has gone directly to the top 5% of households in the United States. Just short of 3% of total economic growth went to the bottom 20% of households, while more than half went to the wealthiest 20%. Wealth inequality from the late sixties throughout the development of the neoliberal period can be described in one sentence – the rich got richer and the poor get poorer.

The bottom 95% of families have experienced within themselves disproportionate rates of economic growth relative to productivity. While workers are producing more than ever for their bosses, hikes in productivity in the neoliberal period haven’t resulted in higher wages at all. Drew DeSilver has pointed out in his work through the Pew Research Center that while productivity amongst workers has increased by 80% over the past 30 years, the data will show that the buying power of the wages those workers earned has moved up barely a percent and a half. Despite this near doubling in productivity, neoliberal austerity and market purism have made more money than ever for those at the top, and stolen more than ever from those at the bottom. The general tendency of money to move upwards on the capitalist market has resulted in exponential gains for the ultra-rich, which as mentioned before, creates an exponential increase in the buying-power of the rich and a stagnating or decreasing buying-power of the poor.

Alongside the hikes in productivity and slow growth of wages, nearly 80:1 from 1987-2017, there has been a drastic shift in employment by major industry sector amongst the total workforce. From 1948-1975, the total employees in the United States increased by 65.67%, around 2.43% annually. From 1975-2017, total employees increased by 79.23%, or 1.89% annually. Even though productivity and total wealth increased exponentially over the neoliberal period, employment decreased in growth year after year.

Amongst the general change in total employment, specific industries saw drastic changes during the neoliberal period compared to the period of government intervention policy stemming from the FDR era. Manufacturing jobs have disappeared in mass numbers since the beginning of the neoliberal era. Manufacturing has been pushed abroad to keep up with the ‘cutting costs’ doctrine of neoliberalism, while more workers than ever are forced into low-paying service and information jobs, since these are the only jobs that exist anymore. Retail positions have increased proportionally with total employment, but many of these positions are occupied by formerly well-employed manufacturing jobs. The shift in employment by major industry sector can be observed as a primary vehicle for the slow-growth of working-class buying power, as well as an expression of ever-disappearing manufacturing jobs.

In terms of buying power of the working-class, the numbers represent a similar transformation of shares of economic expansion, though the buying-power can illuminate a more concrete examination that accounts for the bourgeois notion of inflation and market behaviors.

From 1967 to 2017, the buying power of the lowest 80% of families grew at a similar rate to the actual dollar amount in the previous data set. From a sliding scale of the least to most wealthy in terms of economic expansion, the buying-power of the poor increased by around half compared to their dollar-amount wages while the buying-power of the wealthiest percentile classes increased by around 2.1 times. Though these numbers from the census do adjust buying power to examine the market behaviors and adjust the wages to paint a more accurate picture using consumer price indexes, these numbers are not adjusted to account for factors that only affect growth amongst the ultra-rich, i.e., debt, investments, property, etc. Furthermore, the tendency of capital upwards results in exponential increases in the buying-power of those at the top, but commodities can only grow so expensive before those at the bottom can no longer pay for them, thus the tendency of the rate of profit to fall despite exponential levels of expansion for the most-high spheres of capital.

Of course, the most wealth 5% of households in the United States have enjoyed economic expansion that dwarfs that of those at the bottom, a near 60-40 split. This is largely due to the existing ownership of the means of production and investment spheres by the ultra-rich maintaining their positions through one of the largest hikes in productivity in the history of capital itself. The bureau of labor statistics provides us with a catalogued measure of productivity increases by major industry sector, though some catalogs only go back as far as 1987. Despite this, the numbers are still useful to examine the production and profitability levels of economic industry relative to real wage increases.

There are data series on productivity in the manufacturing sector using the same measuring scale as the data set above, though the historical series only date back to 1987, presenting several problems, but the data itself is still very useful. The data is included in the above chart, though 1967-1986 are omitted for mentioned reasons.

Referring to the real average household incomes of the same time-set discussed above, we can build a relationship by percentile class of the wage-productivity increase from 1967-2017. Listed below are both the data from 1967-2017 as well as a smaller section from 1987-2017 to include manufacturing data relative to the other major industry sectors.

Regardless of year and industry, there is a general tendency both within the latent capitalist mode of production as well as the neoliberal tendency for exponentially disproportionate ratios of growth to productivity depending on income class. Since 1987, there has been a harsh stagnation of wages especially amongst the poorest 20% of households in the United States that was not shared in years prior. Following the tendency of the income-productivity relationship upwards can illuminate the fact that the neoliberal period has resulted in the richest few in the United States have received the overwhelming majority of money and buying-power from the bottom. The philosophy of trickle-down economics combined with the furthering development of the capitalist tendency towards class-monopoly has resulted in both the longest period of wage stagnation in the history of American capitalism as well as the largest wealth inequality in the history of this country. Hikes in productivity are useful for examining the rate at which working-class wages are outpaced by economic growth, but these productivity measures also help illuminate the mass-level of accumulation and theft that the billionaire class has taken part in over the past 50 some-odd years.

In all industries, sans manufacturing, the highest 20% of household incomes have reaped the rewards of the increased productivity of the bottom 80%. The outsourcing and evisceration of American manufacturing deals primarily with the need for a higher profitability from labor by those who own the manufacturing means, as well as the systemic decline in union membership and labor solidarity from Reagan to present. Furthermore, the top 5% of families have almost exclusively reaped the rewards of hikes in productivity, being the only percentile class in the country that has achieved a level of economic growth that is even barely comparable to the growth of productivity. Again, this wage-productivity relationship only grows more dramatic and exponential as you examine those higher and higher up on the wealth ladder. For those at the very top, their economic growth makes that of those of the bottom 99% seem like raindrops in the vast open ocean.

In the period of FDR, there were three solutions to the crisis of capitalism across the world – Bolshevism, fascism, and social-democratic government policy. If the policy of FDRs social-democratic platform was to sustain the rate of profit through bailing out the worker through mass government programs, the policy of neoliberalism was to simply allow the economy to bottom out, so that the rate of profit could be restored organically in the market. The neoliberal period which proceeded from the welfare state allowed for mass accumulation of capital by the ultra-rich at exponential levels. In the early 20th century, bailing out the ultra-rich would not allow for an organic recovery of the rate of profit since the raw inequality between the rich and poor paled in comparison to that of the 21st century. However, in 2020, the capitalist system has been able to sustain its profits by doing precisely what couldn’t be done 100 years ago – bailing out the 1% of the 1% time after time. The capital that has been accumulated in disproportionate amounts over the past 100 years has facilitated this very process of the reintroduction of mass government programs that serve the market, only this time, they serve those at the top instead of those at the bottom. The program of neoliberalism is the death knell of capital, whose only defense is to consume its very mechanism of its own creation and sustenance.

The rate of profit is in decline. There are two paths forward from neoliberalism. The first path is the possibility that capital can save itself through the false-promises of several decades of social-democratic reform, recreating the conditions that led to the development of neoliberalism. The second path is the dissolution of capital by its own hand. Capitalism has dug its own grave through the doctrine of neoliberalism, resulting in the greatest wealth inequality in the history of capital and the ever-growing contradictions of labor and productivity. The path forward from the death knells of capital cannot be understood as some sort of communist eventuality. Capital will certainly die, but what takes is place is certainly indeterminate.

Neoliberalism has wreaked havoc on the worker for half a century now. Corporate tax cuts, the starvation of the worker, and the greatest wealth inequality the country has ever seen – these are the legacies of neoliberalism. Its doctrine has been nothing but the largest heist in the history of capitalism, with the ultra-rich stealing more every day from the pockets of the worker. The path forward must address these concerns, lest we allow the economy to bottom out, and leave authoritarianism and failed bourgeois economics to dominate the world as it has for the past century.

Thomas McLamb is a Lebanese-American Marxist writer, historian, and graduate student residing in the so-called United States. Thomas has spent the last few years researching historic wages, economic expansion, recession, and the currents of capitalism both in the so-called United States as well as internationally.