Pictured: A Maricopa County constable escorts a family out of their apartment after serving an eviction order for non-payment on Sept. 30 in Phoenix. [John Moore / Getty Images]

By Shawgi Tell

One of the fundamental economic laws under capitalism is for wealth to become more concentrated in fewer hands over time, which in turn leads to more political power in fewer hands, which means that the majority have even less political and economic power over time. Monopoly in economics means monopoly in politics. It is the opposite of an inclusive, democratic, modern, healthy society. This retrogressive feature intrinsic to capitalism has been over-documented in thousands of reports and articles from hundreds of sources across the political and ideological spectrum over the last few decades. It is well-known, for example, that a handful of people own most of the wealth in the U.S. and most members of Congress are millionaires. This leaves out more than 95% of people. Not surprisingly, “policy makers” have consistently failed to reverse these antisocial trends inherent to an obsolete system.

At the same time, with no sense of irony and with no fidelity to science, news headlines from around the world continue to scream that the economy in many countries and regions is doing great and that more economic recovery and growth depend almost entirely, if not entirely, on vaccinating everyone (multiple times). In other words, once everyone is vaccinated, we will see really good economic times, everything will be amazing, and we won’t have too much to worry about. Extremely irrational and irresponsible statements and claims of all kinds continue to be made in the most dogmatic and frenzied way by the mainstream press at home and abroad in a desperate attempt to divert attention from the deep economic crisis continually unfolding nationally and internationally. Dozens of countries are experiencing profound economic problems.

While billions of vaccination shots have already been administered worldwide, and millions more are administered every day (with and without people’s consent), humanity continues to confront many major intractable economic problems caused by the internal dynamics of an outdated economic system.

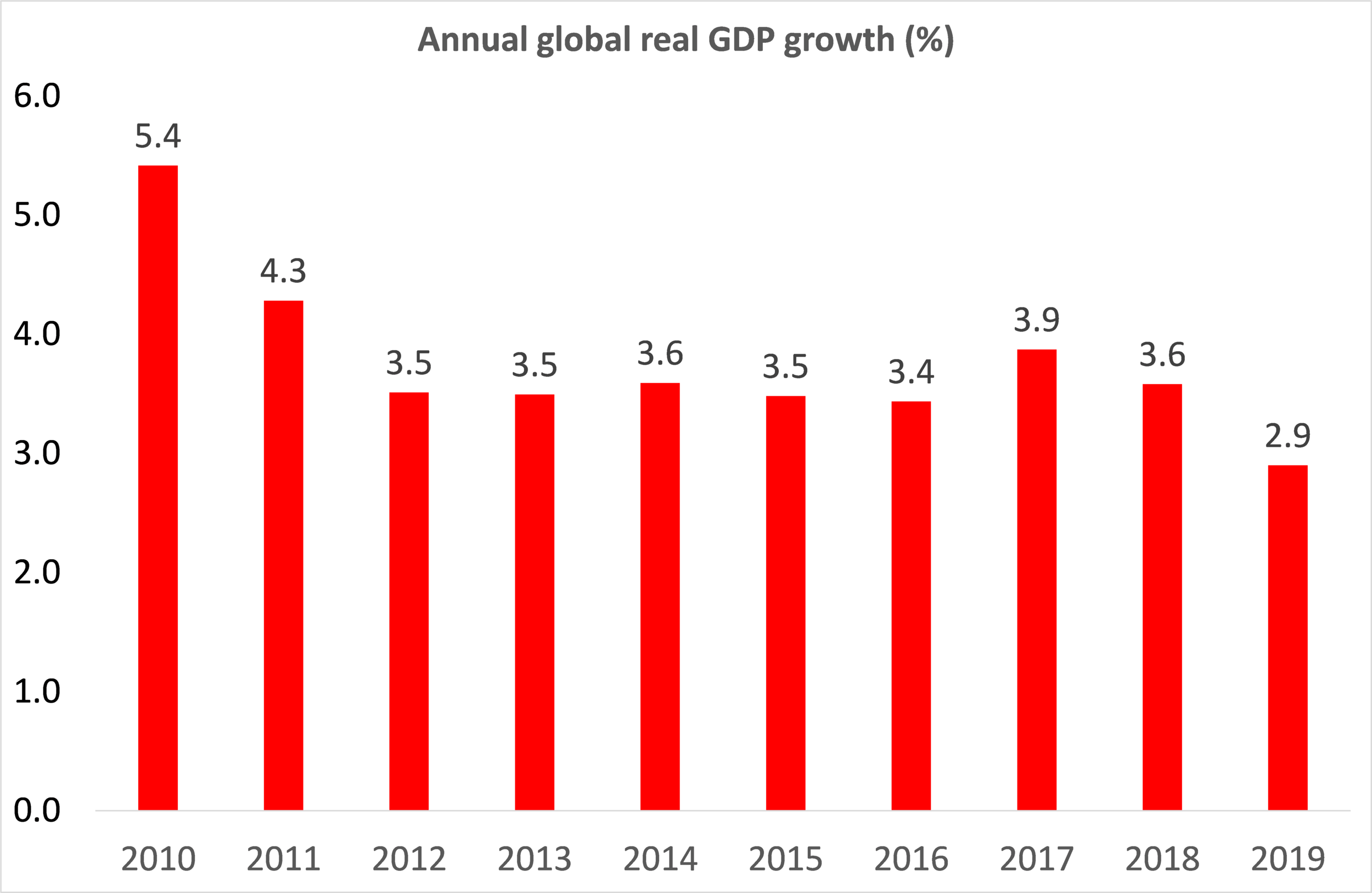

A snapshot:

1. More rapid and intense inflation everywhere

2. Major supply chain disruptions and distortions everywhere

3. Shortages of many products

4. “Shortages” of workers in many sectors worldwide

5. Shortened and inconsistent hours of operation at thousands of businesses

6. Falling value of the U.S. dollar and other fiat currencies

7. Growing stagflation

8. Millions of businesses permanently disappeared

9. More income and wealth inequality

10. High dismal levels of unemployment, under-employment, and worker burnout

11. Growing health insurance costs

12. Unending fear, anxiety, and hysteria around endless covid strains

13. More scattered panic buying

14. The stock market climbing while the real economy declines (highly inflated asset valuations in the stock market)

15. Spectacular economic failures like Lehman Brothers (in the U.S. 13 years ago) and Evergrande (in China in 2021)

16. All kinds of debt increasing at all levels

17. Central banks around the world printing trillions in fiat currencies non-stop and still lots of bad economic news

18. And a whole host of other harsh economic realities often invisible to the eye and rarely reported on that tell a much more tragic story of an economy that cannot provide for the needs of the people

The list goes on and on. More nauseating data appears every day. Economic hardship, which takes on many tangible and intangible forms, is wreaking havoc on the majority at home and abroad. There is no real and substantive economic improvement. It is hard to see a bright, stable, prosperous, peaceful future for millions under such conditions, which is why many, if not most, people do not have a good feeling about what lies ahead and have little faith in the rich, their politicians, and “representative democracy.” It is no surprise that President Joe Biden’s approval rating is low and keeps falling.

What will the rich and their political and media representatives say and do when most people are vaccinated, everyone else has natural immunity, and the economy is still failing? What will the rich do when economic failure cannot be blamed on bacteria or viruses? To be sure, the legitimacy crisis will further deepen and outmoded liberal institutions of governance will become even more obsolete and more incapable of sorting out today’s serious problems. “Representative democracy” will become more discredited and more illusions about the “social contract” will be shattered. In this context, talk of “New Deals” for this and “New Deals” for that won’t solve anything in a meaningful way either because these “New Deals” are nothing more than an expansion of state-organized corruption to pay the rich, mainly through “public-private-partnerships.” This is already being spun in a way that will fool the gullible. Many are actively ignoring how such high-sounding “reforms” are actually pay-the-rich schemes that increase inequality and exacerbate a whole host of other problems.

It is not in the interest of the rich to see different covid strains and scares disappear because these strains and scares provide a convenient cover and scapegoat for economic problems rooted in the profound contradictions of an outmoded economic system over-ripe for a new direction, aim, and control. It is easier to claim that the economy is intractably lousy because of covid and covid-related restrictions than to admit that the economy is continually failing due to the intrinsic built-in nature, operation, and logic of capital itself.

There is no way forward while economic and political power remain dominated by the rich. The only way out of the economic crisis is by vesting power in workers, the people who actually produce the wealth that society depends on. The rich and their outmoded system are a drag on everyone and are not needed in any way; they are a major obstacle to the progress of society; they add no value to anything and are unable and unwilling to lead the society out of its deepening all-sided crisis.

There is an alternative to current obsolete arrangements and only the people themselves, armed with a new independent outlook, politics, and thinking can usher it in. Economic problems, health problems, and 50 other lingering problems are not going to be solved so long as the polity remains marginalized and disempowered by the rich and their capital-centered arrangements and institutions. New and fresh thinking and consciousness are needed at this time. A new and more powerful human-centered outlook is needed to guide humanity forward.

Human consciousness and resiliency are being severely tested at this time, and the results have been harsh and tragic in many ways for so many. We are experiencing a major test of the ability of the human species to bring into being what is missing, that is, to overcome the neoliberal destruction of time, space, and the fabric of society so as to unleash the power of human productive forces to usher in a much more advanced society where time-space relations accelerate in favor of the entire polity. There is an alternative to the anachronistic status quo.

Shawgi Tell, PhD, is author of the book “Charter School Report Card.” His main research interests include charter schools, neoliberal education policy, privatization and political economy. He can be reached at stell5@naz.edu.